For landlords, these policies protect them from financial losses when damages stem from cases of renters’ liability. For renters, coverage is primarily for unit damage resulting from covered perils, and protection for losses related to their personal belongings. In 2022, the average renters insurance policy came out to be ~$18.00 per month with only a $500 deductible.

Since many property or business policies have high deductibles averaging around $100,000, claims under that amount would likely be an out-of-pocket expense for the landlord. If a claim exceeded the deductible, a landlord would still be responsible for the amount up to their deductible.

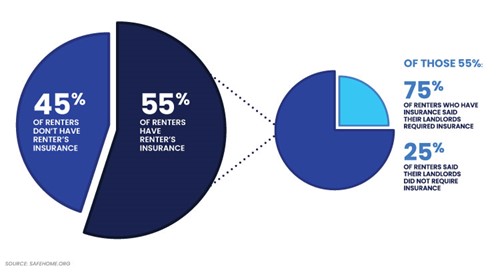

Requiring renters insurance seems like a no-brainer, so what are the problems?

This requirement creates extensive work for property management staff. To start, properties are required to be listed as a named insured on the insurance policy. If property managers allow a resident to move in without a policy, the managers may have to hound them for it. If a property takes a more stringent approach, preventing the resident from moving in without a policy, it could cost the property a valuable lease-up or move-in.

Even in the cases when a proper renters insurance policy is obtained and provided to the property, many renters insurance policies lapse for non-payment or are intentionally canceled by the resident during the lease term. Unbeknownst to the landlord, there would be no coverage in the case of an incident, potentially resulting in financial loss.

There are solutions offered now that reduce the administrative burden of monitoring renters insurance compliance while also ensuring all units are covered at all times.

Many solutions out there assist in the collection of third-party policies. However, their capability to monitor the active status of those policies daily is often lacking. When the responsibility of monitoring is put on your site staff, it introduces heavy manual work and creates a less-than-ideal relationship for your residents and property managers. Additionally, your risk exposure increases daily as you wait for residents to turn in an updated policy, if ever. This leads to unnecessary risk exposure at the property level. With a high number of residents lapsing and canceling their coverages, it’s important to have an automated solution in place to assist in tracking and to guarantee 100% coverage.

What do I do now?

Find a solution to implement that aligns with your company goals.

What does a good solution look like?

- A good solution offers easy enrollment while promoting high absorption. With low-action residents, an opt-out model works best.

- Ongoing tracking and monitoring of 3rd party policies is key. If you are not monitoring the active status of all policies, residents will slip through the cracks and expose you to risk.

- Automation is critical to 100% compliance. A strong solution can automatically place residents on liability programs if a lapse occurs.

- Remove site-level tasks. The more manual the process, the more risk you’re exposed to. By removing these tasks, you allow staff to focus on core responsibilities and lower risk exposure.

- Integration matters. If your solution doesn’t integrate with PMS, it falls on your site-staff to manage, track, and collect.

- Seamless management of claims. Find a solution that understands the complexity of claims processing and works to turn units around quickly.

- A great solution grows with you. As your business continues to evolve, choose someone who can come along for the ride and provide their solution across multiple PMS platforms as well as captive scenarios.

These solutions are incredibly helpful, but what if I want to self-insure?

For multifamily groups of a certain size, a captive is a fantastic way to financially benefit through self-insuring. Due to a favorable loss ratio, the world of renter’s liability is a nice entry point into captives. If your business is willing to take on that risk now or in the future, find a solution that can transition into various scenarios. Regardless of your growth, risk profile, or business goals, ensure you have a partner in place who continues to provide the tracking and monitoring of policies as well as administrative services to guarantee 100% coverage.

For multifamily properties of nearly all sizes, the ability to monitor insurance coverage can completely change the experience for both property managers and residents. Whether it’s preventing lapses in coverage, avoiding financial losses, freeing up more time for site-level staff, or simply ensuring residents aren’t left watching over their policy unaided, there’s little question that a well-implemented renters insurance alternative can offer a range of benefits. With a wide variety of potential solutions out there, we hope we’ve shed some light on how using a strong rubric or set of criteria can help you find the best potential partner in coverage.

Author Bio

Sarah Creighton is Vice President of Sales and Business Development at Foxen, a real estate technology company dedicated to creating solutions that benefit both properties and their residents.

At Foxen, Sarah has established and implemented strategic initiatives across sales, operations, and IT divisions, leading a sales team to consistent year-over-year growth of over 100%.

Sarah brings over 15 years of property management and insurance industry experience, building and managing business development units for companies such as Nationwide Insurance, IGS Energy, and Sogeti.